Nimdzi 100 report

Great Industry insights in the

Nimdzi 100 report

By Laszlo K. Varga and Marjolein Groot Nibbelink

Market Size and Growth

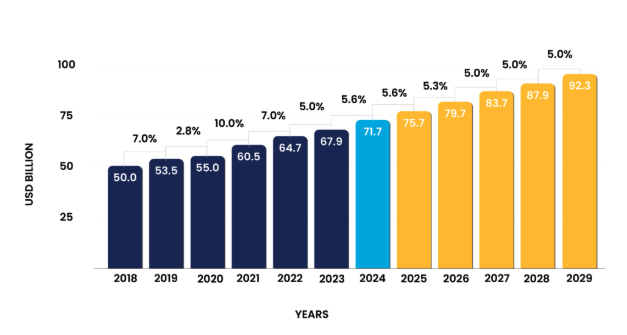

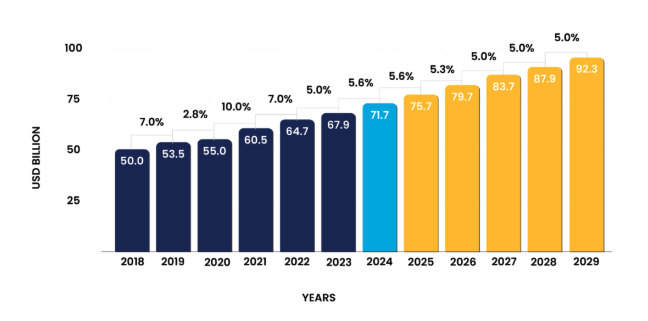

We estimate that the language services industry, with a 5.6% growth, reached USD 71.7 billion in 2024 and projected it to grow to USD 75.7 billion in 2025.

Instead of the pre-AI compound annual growth rate (CAGR) of 7.0%, we adjust our future prediction downwards to a more linear growth in the near future and a slower, 5.0% CAGR afterwards. We project that the industry will reach USD 92.3 billion by 2029.

The combined revenues of the top 100 positions in this year’s ranking increased by 6.0% compared to last year’s 5.0%. The top 50 positions showed the highest increase of 6.6% in compound revenues.

This year’s top 10 ranked companies grew by an average of 5.2% compared to their last year’s revenue, thanks to Propio’s remarkable entry into the top 10 after significant acquisitions.

The language industry: Market growth 2018-2024 and forecast 2025-2029

Geographical Distribution

Of the top 100 language service providers (LSPs) in this year’s Nimdzi rankings, 41% are headquartered in Europe and 34% in North America. Companies from Asia represent 18% of the geographical distribution. Oceania hosts 7% of the top players. Tarjama entered onto the Nimdzi 100 as the second company from the Middle-East (counted in Asia).

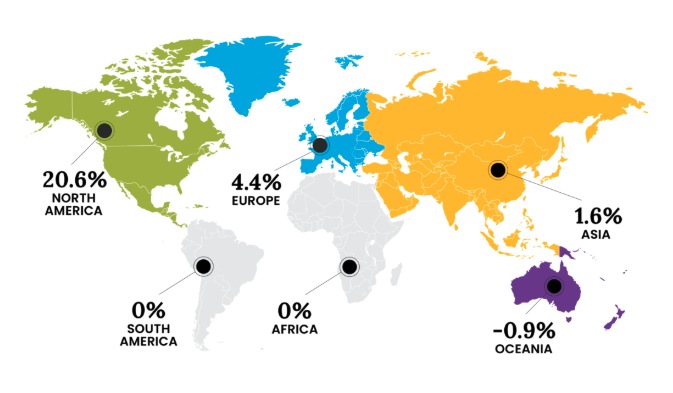

According to the survey results, 45.2% of revenues in 2024 came from clients based in North America (down from 49.9% in 2023), Europe accounted for 34.2% of the client base (down from 38.5% in 2023), and 17.0% of revenues were derived from customers in Asia (up from 12.2% in 2023). South America (1.4%), Oceania (1.9%), and Africa (0.4%) are the smallest – but increasing – regions in terms of client base in 2024.

Growth of the 100 Largest LSPs by Geographical Distribution

Money and Business Environment

Machine translation (MT) and post editing, data services, prompt engineering and pure technology offerings accounted for the greatest increase in revenues from 2024 – a nod to the quick evolution of artificial intelligence (AI) tools.

Growth verticals are those with traditionally large capital flow – healthcare, private entities, government, financial, and legal.

The need to increase revenue and dealing with price pressures are reported as top three most important business challenges from 2024.

50.0% of Language Service Providers (LSPs) expect a continuation of their Q4 2024 revenue growth into 2025, proof of industry stability and business opportunity.

The U.S. election, continuing mass migration, and armed conflict in Europe have contributed to market hesitation.

The easing of inflation during 2024 and into 2025 as well as the reduction of interest rates encourage investment.

Strategic investments are being made to continue reducing office space (25.9% up from 17.8%), cut in-house staff (26.9% up from 13.2%), and increase the use of MT (69.4% up from 63.6%).

The global trade war is likely to reduce cross-border product volumes but the number of products may be less affected, leaving plenty of translation work to be done.

Business situations in Q4 of 2024 were reported by 88% of LSPs as being satisfactory or good. The anticipation for Q1 2025 sees 82% reporting a satisfactory to good outlook.

Mergers and Acquisitions

Last year we predicted big changes in the top 10 of the ranking. While none of the largest players merged, a new player – Propio – rose to the top ranks thanks to acquisitions of ULG, Akorbi, and ASL Services.

It’s a seller’s market. For at least five years, the interest to buy has outweighed the urge to sell, indicating private investors’ high interest in scaling their business and signaling potential for more deals in 2025 and beyond.

In 2024, the general mergers and acquisitions (M&A) landscape stayed on similar restrained levels as in 2023, and the AI confusion is adding to the complexity in the space.

Many of the industry’s M&A activities were about in-trade acquisitions and mergers. Founder-owned small and mid-size LSPs that struggle with revenues have been looking for exits, triggering consolidation in the middle ranks.

In 2025, M&A in the industry is shifting towards acquiring AI capabilities and revamping localization workflows with generative AI (GenAI) and large language models (LLMs), expanding on the focus of revenue growth or geographic expansion – the traditional reasons for consolidation.

Additionally, the interpreting sector is poised for disruption as real-time speech recognition and machine interpreting (MI) technologies advance, leading companies to seek AI-powered interpreting solutions – even through acquisition. Traditional interpreting LSPs are looking to stay ahead of the disruption curve, and we are already seeing this with the recent acquisition of sign language AI tools by Sorenson.

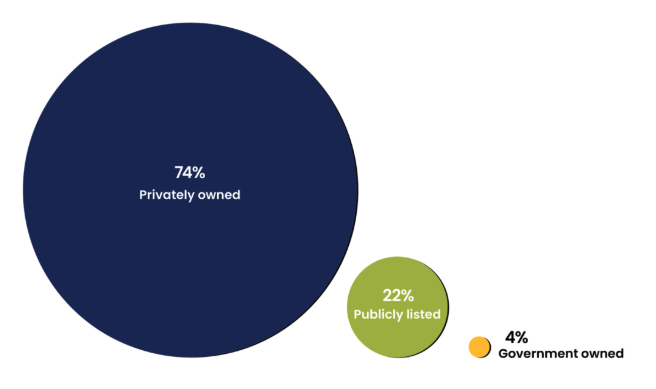

LSP Ownership Type Distribution

Key Trends

GenAI and LLMs have a green light. 2024 was the second full year of GenAI. Tech-forward LSPs shifted from defense to offense, creating AI platforms and offering AI-related services, ditching the “machine translation is where it’s at” mantra of the last few years. That said, human cultural and language expertise in supply chains is more valuable than ever.

Client-side AI maturity is increasing. Solid history with using machine translation no longer counts as a competitive factor for service providers. Buyers expressly look for AI-driven features and workflows with expert support from their provider partners. Innovation capability with AI is becoming the number one indicator of future partnerships for LSPs and language technology providers (LTPs) alike.

The traditional bread-and-butter translation work is diminishing. Service providers that rely on subcontracts in long supply chains and on traditional translation services struggle to maintain their value proposition. In addition, many small and medium enterprises lack the data, understanding, and maturity to embrace human-in-the-loop localization in the much hyped AI world. This will lead to many small founder-led LSPs’ struggle in the new AI era and the sale or closure of their business.

Tech-forward LSPs have the competitive edge. Mid-size tech-enabled LSP contenders have a great opportunity with AI technology stacks to grab market share from the top ranks. And indeed, providers such as Translated, Lilt, Smartling, or Argos are capitalizing on their advantage where revenue cannibalization is not a threat to them. The largest players protect their positions with their newly created language AI platforms – Opal, Lia, Lara, Evolve, Aurora, or MosAIQ are all part of this chessboard.

The industry is multi-speed. On the provider side, technology capabilities – which scale with size – seem to define future success. Smaller LSPs are reportedly less positive about GenAI’s impact than they were a year ago, while the larger the company, the more comfortable they are in the new AI era. Over to buyers, a similar divide is visible: many still grapple with core language technologies such as a translation management system (TMS) or MT, while more mature enterprises are eager to invest into AI – and learn how others do it.

Good enough is just good. Enough. The highest language quality is less and less relevant for buyers for most content types. The acceptance bar is being lowered for non-business critical multilingual communications, partly thanks to LLMs’ deceptively fluent output. However, most organizations still struggle with identifying the right content quality tiers. The acceptance bar is being lowered for non-business critical multilingual communications, partly thanks to LLMs’ deceptively fluent output.

Competition is shifting. In platforms from Adobe and Salesforce through Shopify and Canva to Hubspot and MS Office, GenAI-based copilots are offering translation-like features. While all big tech firms are integrating LLMs into their software as a service (SaaS) platforms, these are not ‘localization-ready’ for enterprise purposes – yet.

AI data services are growing – and so does the need for AI model training. Data collection, annotation, validation are offered by practically all tech-savvy LSPs, sometimes even under a specific brand name – RWS TrainAI, Welo Data, Uber Scaled Solutions, or Centific Flow, just to mention a few options.

Technology reduces unit prices – and increases demand. Generic technology alone doesn’t solve the language problem for enterprises, but tools such as MT quality estimation (MTQE) and automatic post editing (AutoPE or APE) increase what we lovingly refer to as leverage (the part of work that does not need a human touch). As price per word continues to decrease, we are approaching the elastic part of the demand curve. This means the overall need for human work will keep increasing as more content can jump the previously high human-in-the-loop cost bar.

Profits can be more important than revenues. Even those LSPs with shrinking demand report stable or increasing margins. This is largely due to advances in workflows and new-found production efficiencies, and a coinciding increased appetite for quality risks on the client side.

Multilingual content creation is not ready to break paradigms. LLMs enable a new disruption for the traditional create-translate-publish content cycle. Demand for AI-powered content creation and post-editing (for certain content types) is slowly picking up – often labeled as AI transcreation or AI content generation. LSPs’ AI platforms inherently offer this as an option, and so do technology providers such as Lilt Create or DeepL Write. However, widespread adoption is not yet seen.

Interpreting will continue (?) to be a growth driver. Demand for interpreting relies just as much on economic factors as on geopolitics, and AI impacts it less (except for niche use cases). In times of crisis – such as war, immigration surges, or public health issues – the need for accurate communication increases. However, language access and equity are under increasing pressure in the U.S., as political efforts chip away at federal enforcement of longstanding legal protections. The erosion of these safeguards could reshape demand for interpreting services across the public sector.

There's high competition for – and a shortage of – top language talent. Price pressure is making the field less attractive to new talent, and while academic programs are offering fewer opportunities for formal training, enrollment numbers have been declining for years. At the same time, requests from buyers are becoming more specific and demanding, particularly in high-impact areas like healthcare and transcreation. Vendor managers are already struggling to fill top-tier expertise roles even in top-tier languages such as Japanese, Korean, and German. These shifts suggest the industry may soon face a broader talent shortage challenge, unless pricing models are adjusted and modernized.

LSP Challenges and Actions

With demand rebounding, 50% of respondents expect an increase in revenues, and a reserved optimism is holding steady across surveyed LSPs regardless of last year’s results.

Growth, innovation through technology, and price pressure are the main business challenges of providers in 2024, same as in 2023.

Cost-saving actions in the next year will shift to implementing more MT and reducing staff and consequently office space as LLMs reshape the evolution of language services.

More than three quarters of LSPs say they have – or are looking into – changing their pricing models from per-word to something else, and only 15.1% say per-word pricing still works.

Change in growth paths in challenging times calls for refreshing leadership ranks. The industry saw seven incoming chief executive officers (CEOs) at Nimdzi 100 ranked LSPs in Q4 of 2024 alone.

State of the Language Industry for 2025

Confusion Amidst New Uncertainties

Undoubtedly, buyers and providers alike are eager to capitalize on the advancements of new language AI tools. Last year saw the birth of many language-focused AI platforms on the provider side, while buyers are pressed from C-level to adopt AI fast and broadly – but there is no clear path paved with repeatable success stories. Although inflation rates stabilized last year globally, many new challenges impacted the industry. Europe, the second largest market for language services, continued to face war in Eastern Europe, high energy prices hampering industrial productivity, and a fragmented regulatory and administrative environment restraining innovation and investment. The U.S. kept and keeps pushing for AI dominance with China being the contender, and the American economy – the largest market for language services – has shown remarkable resilience with low unemployment rates and sustained consumer spending.

2025 doesn’t offer itself to be much different than last year. While a more focused approach to AI automations is expected across the industry spectrum, global and regional economic and geopolitical factors in 2025 will provide no less risks to enterprises and organizations of all scales, clouding the trajectory of our industry. Changes in leadership in the U.S. and (most recently) in Germany, unprecedented tariff wars that seriously challenge globalization and international trade, reduced development aids by the U.S., and booming AGI hype amidst commoditization of foundational AI models fueled by China all add to the complexity of the backdrop LSPs must navigate.

Throughout 2024, many of our discussions with LSPs of all sizes indicated that the year was a mixed bag of nuts. Some reported shrinking demand from clients and declining revenues. Others shared stories about growth in the midst of increasing volumes coupled with lowering per-word rates. The consensus, however, was increased or stable profitability, with the two main factors being new-found production efficiencies and clients’ higher appetite for quality risks. Undoubtedly, progress in technology such as AI and automations results in decreasing unit prices – the metric easiest to compare across offers from a buyer perspective. Tools such as MTQE and AutoPE increase what the industry lovingly refers to as leverage, further commoditizing the typical word-based business models of translation companies. This commoditization largely hinders innovation in operational models, creating a vicious circle where LSPs’ ability to offer gradually higher per-word discounts is a key selling point with less and less room for reinventing the value propositions. Language services are still in the back seat when it comes to enterprises’ business-critical metrics such as faster time-to-market, revenue growth, increased conversion rates, or elevated brand engagement. It remains to be seen whether we see the first LSPs to successfully move to value-based, outcomes-driven pricing, especially in the face of resistance from clients. The ongoing disruption by AI might just provide the right backdrop for such business model innovation.

Profitability Change in 2024

The consensus was increased or stable profitability, with the two main factors being new-found production efficiencies and clients’ higher appetite for quality risks.

Ready. Set. AI?

AI, of course, remains a central topic of discussions and debates on all levels of the economy, especially in the context of the job market. The vision of AI labs and tech providers that generative AI will overtake jobs and diminish the need for human expertise in most white-collar professions has not (yet) come to realization. For instance, software development companies – a much larger sector than translation – have not implemented wide-spread layoffs, even though AI coding copilots as a potential market are much more in the focus of AI labs than the ‘language challenge’ in which our industry specializes. In addition, a recent study by Microsoft and Carnegie Mellon showing that an overreliance on AI may reduce workers’ ability for critical thinking is a warning sign that there are complex human factors to consider when incorporating AI into workflows.

While many menial tasks are automatable by AI, the value created by humans is more than just a sum of tasks: subject matter expertise, decision making, learning and development, and – most importantly – empathy and reasoning are components that AI systems can’t yet replicate. In the language services space, the integration of AI into localization processes keeps being gradual as a feature rather than a disruptive new way of working. On the large scale, AI tools complement rather than replace existing workflows, technologies, and human skills.

That said, AI with language capabilities is gradually making its way into our everyday personal and business lives. In platforms from Adobe and Salesforce through Shopify and Canva to Hubspot and Microsoft Office, GenAI-based copilots are offering translation-like features. While all big tech firms are integrating LLMs into their SaaS platforms, these are not ‘localization-ready’ for enterprise purposes – yet. As long as users can’t verify the correctness of the content transformed by machines, the output is no more than “(pre-)translation.” Nevertheless, the gradual improvement of LLMs predicates that competition is shifting for non-critical content.The promise of and interest in AI is not subsiding as users (and decision makers) find tangible benefits such as near-instantaneous results, acceptable-looking output quality, and 24/7 availability highly compelling. This, in turn, makes the case that LTPs are seen as competition to LSPs in providing services. Companies like DeepL and Weglot deserve a seat on our rankings, while tech-focused LSPs such as Translated, Lilt, and CQ Fluency showed growth multiple times higher than the average. The line between technology and service providers is blurring thanks to the abundance of use cases enabled by AI, further adding to the confusion across the market.

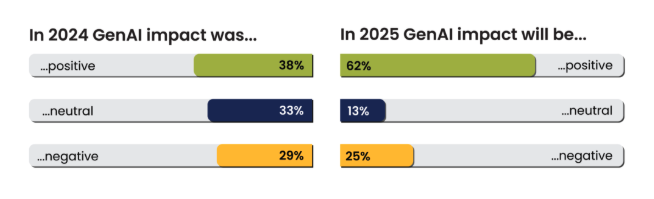

How LSPs Expect GenAI to Impact Their Business

Still a Growing Industry

In 2024, we estimated that the industry will pick up the pre-AI growth level of 7.0% annual growth rate. Our research prompts us to correct our previous projections downward. We now adjust this picture to project a more linear growth in the near future and a slower, 5.0% CAGR afterward. This estimation, of course, has a lot of uncertainty, and the range of possible growth outcomes are heavily dependent on technology as much as economic factors. Whether AI efficiency gains and lower per-unit prices will reach a level where demand becomes elastic and boosts overall market growth to pre-AI levels remains to be seen, but the industry has the ability to successfully navigate these challenges, and our research supports this confidence.

We estimate that the language services industry reached USD 71.7 billion in 2024 and project it to grow by 5.6% to USD 75.7 billion in 2025.

The results of the Nimdzi 100 research indicate that growth across the spectrum of LSPs was slightly stronger in 2024 than in the year before. The more traditional players – such as Transperfect, RWS, Lionbridge, and Welocalize – show varying results with single percentage point changes up or down. Equally mixed results are seen from the LSPs mostly engaged with the entertainment sector – Iyuno, Dubbing Brothers, and Plint on the less fortunate side, while ZOO Digital and Pixelogic report strong performance especially compared with 2023. In addition, a select few mid-tier LSPs have seen a slip in their standings, either descending the ranks or finding themselves on Nimdzi's watchlist.

Remarkable success stories are also visible from the results. LanguageLine became the second-ever LSP to cross the USD 1 billion revenue mark, Keywords Studios is close behind having moved two rungs up the ladder to 3rd position with impressive growth in the gaming sector, Propio making the top 10 via both the acquisitions of Akorbi and ULG as well as organic growth in interpreting. The successes of LSPs such as AMN, Global Talk, GLOBO, ElaN, Equiti (formerly Cloudbreak and Martii), and DALS (formerly DA Languages) continue to demonstrate robust performances in specific segments like interpreting, healthcare, and public sector engagements. Toppan and PGLS continued to see their performance fueled by regulatory demands for comprehensive language access. 2024 also saw strategic movements through M&A, especially as language technology has become a main interest for investments, and profitability in the sector is stable or improving.

We see two focus areas of growth for the foreseeable future. First, interpreting will continue to be a growth driver. Demand for interpreting relies just as much on economic factors as on geopolitics. In times of crisis – such as war, immigration surges, or public health issues – the need for accurate communication increases. However, language access and equity are under increasing pressure in the U.S., as political efforts chip away at federal funding for multilingualism, having declared English as the official language on federal level. The good news is that interpreting is still a human profession, with all its quirks and opportunities. Hourly and daily rates of interpreters are only expected to increase as technology does not solve the problem of replacing human interpreters entirely. That said, AI is seeping into interpreting in two ways: it can help reduce the need for human involvement in non-critical discussions (for instance, with appointment booking interactions in patient journeys) and providing – limited but useful – multilingual support where human interpreters are not available or affordable.

The second main growth potential resides with tech-forward LSPs, especially mid-size contenders who have a great opportunity with AI technology stacks to grab market share from the top ranks. And indeed, providers such as Translated, Lilt, Smartling, or Argos are capitalizing on their advantage where revenue cannibalization is not a threat to them. The largest players protect their positions with their newly created language AI platforms – Opal, Lia, Lara, Evolve, Aurora, or MosAIQ are all part of this chessboard. AI-driven custom solutions cut per-word translation costs by up to 40%, increasing efficiency to a level that enterprise procurement teams can’t ignore – even if these products may still require significant investment for enterprise-wide deployment as they are not immediately plug-and-play with existing content systems.

The language industry: Market growth 2018-2024 and forecast 2025-2029

Reserved Optimism and Projections

Not all boats are lifted by the tide. We hear the voices of those who ask us “How can the industry grow by 5-7% if my business is struggling?”, and while the answer is not simple, growth data by size and segment provide insights into this. The top 50 ranked LSPs show the largest average year-on-year growth (close to 6.6%), while the aggregate results of those LSPs below the 100 line are closer to 2-3%. There are multiple reasons behind this growth asymmetry, including:

Providers’ ability to harness technology depends on the level of scale, as the new language AI is not directly plug-and-play but requires experimentation, investment, and strong customer focus.

Traditional, founder-owned LSPs, as well as those that rely on indirect work from the largest providers are often limited in their innovation capabilities.

There is a generational shift in the mid- and high-market LSP leadership that is often fueled by private equity (PE) investment. Professional management practices are more likely to lead to higher brand recognition, technology adoption, and more successful sales efforts.

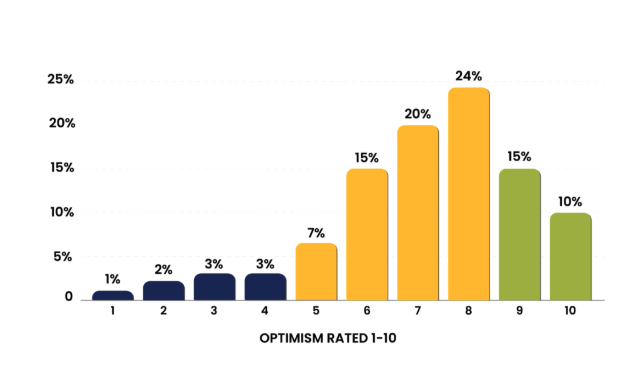

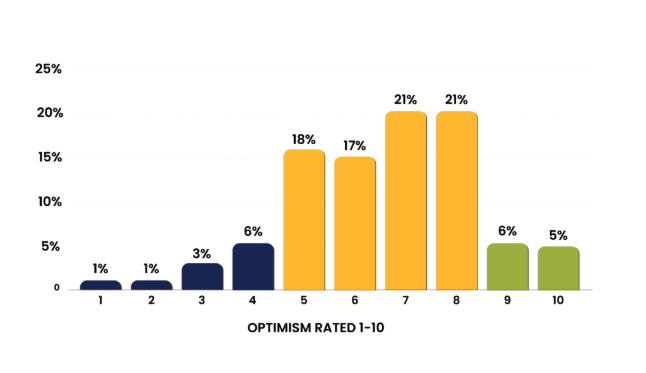

Service Providers’ Optimism About the Industry

Service Providers’ Optimism About Their Company